AML and CFT Guide for Money Transfer Start-Ups

Anti-Money Laundering (AML) and Countering the Financing of Terrorism (CFT), are terms mainly used in the financial and legal industries to describe the legal controls that require financial institutions and other regulated entities to prevent, detect, and report money laundering and terrorist financing activities.

Every regulated entity should have appropriate AML as well as CFT checks and controls in line with the regulatory framework of the jurisdiction where the entity operates from.

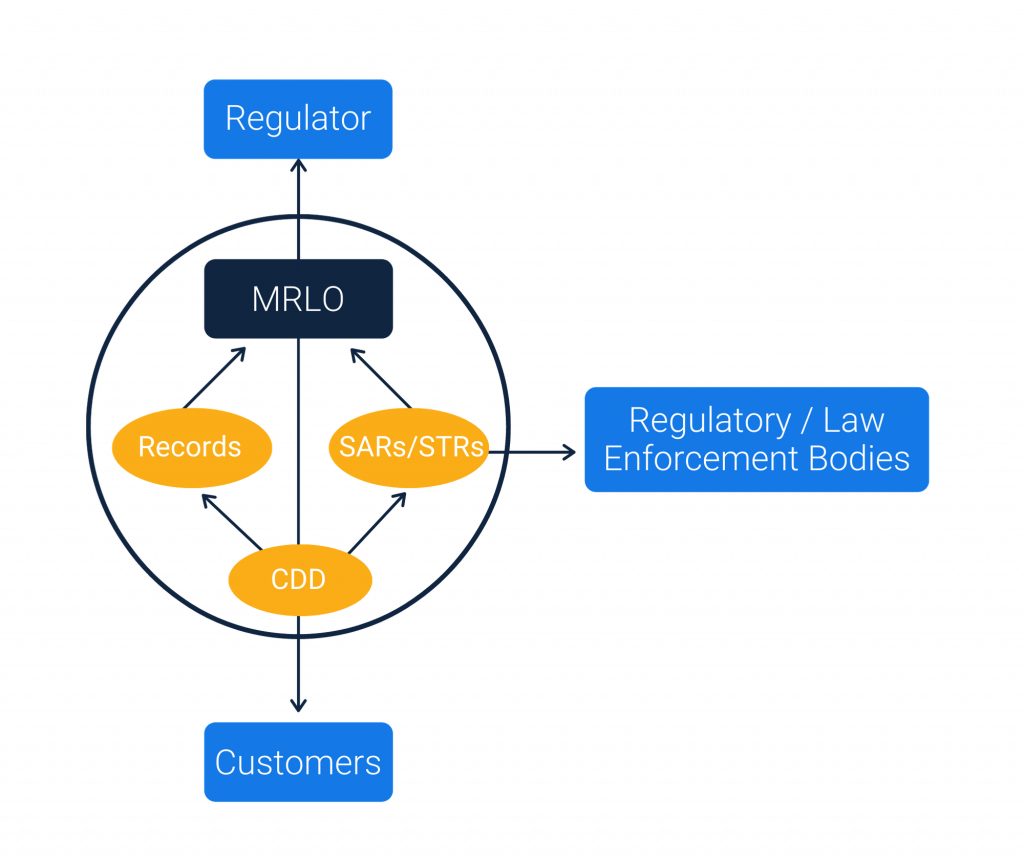

To make it easier for Start-Ups, please find below the diagram of the AML/CFT Ecosystem:

The ecosystem shown above shows the five core responsibilities of Money Transfer Start-Ups:

1. Onboard a Money Laundering Reporting Officer (MLRO)

First and foremost, all start-ups must have a dedicated Money Laundering Reporting Officer (MLRO) who is responsible for managing all compliance activities within the organisation. Depending upon the type and size of the business, there could be one or more members within the compliance team.

Aside from the MLRO, it is important that other stakeholders such as Directors, Senior Managers and even Shareholders familiarise themselves with the Payment Services and AML regulations within the jurisdiction where the business is registered.

2. Customer Due Diligence (CDD)

Each entity is responsible to identify the customers that they deal with. This step is known as the Know Your Customer (KYC). The MLRO has to identify the checks and controls that need to be in place to capture all the information needed from the customers as part of the KYC process.

Apart from KYC, the entity must also maintain the Customer Due Diligence which is mainly to do with checking the customers registering against the watch lists and the transaction patterns of the customers.

3. Suspicious Activity Reporting (SAR)

The entity is required to conduct appropriate investigations whenever an event such as a transaction monitoring alert or a sanctions match occurs. The MLRO has to validate such investigations further and need to report to the local regulatory bodies in the form of Suspicious Activity Reporting (SAR) or Suspicious Transaction Reporting (STR).

4. Record Keeping

The entity is responsible to maintain records of all their customers and transactions for a minimum period of 5 years or as per the guidelines of the local regulatory bodies. The MLRO has to ensure that the data captured from customers for identification and transaction purposes are stored securely and accessible to the authorized individuals of the entity whenever needed. Apart from customers and transactions data, the entity should also maintain the records of all the SARs/STRs.

5. Registering and Reporting to Regulators

The entity is responsible to have the registration done with the relevant regulatory bodies in the jurisdiction where the entity operates from. The entity should also be aware of all the reporting obligations in order to submit reports related to the customers or transactions data to the relevant regulatory bodies in the jurisdiction.

Whether you are a start-up or an established Money Service Business, it is very important that the AML policies and procedures are clearly incorporated within your business model. For more information, advice and support, please contact us.

RemitONE provides proven compliance products for Money Service Businesses and Central Banks and would be delighted to help your business. Contact marketing@remitone.com or call +44 (0) 208 099 5795.

Mobile Money in Africa

Africa is something of an anomaly in the developing world. It’s a continent that many people forget is not a single country but 55 individual countries with dozens of currencies. It’s also a continent where around 66% of the adult population remain unbanked. However, while more than half of the continent has no access to a bank account, the mobile economy is booming. Indeed, Sub-Saharan Africa is the world’s fastest-growing mobile phone market. For the remittance sector, this poses a pretty enticing opportunity.

While the typical customer living out in rural Kenya might live several days away from the nearest bank, they are likely to have direct access to a mobile phone that can be used to send and receive digital payments. This is why the mobile money systems in the region have spread so fast. But how will MTOs cope with increasing digitisation and compliance issues as more customers go online and start using mobile apps to send their money?

To dive deeper into the current mobile money climate in Africa, RemitONE Associate Sales Director Oussama Kseibati recently hosted a webinar attended by esteemed panelists with expert knowledge of the regional remittance landscape. Muhammad M. Jagana, CEO of Kuringo, Sidharth Gautam, Head of Sales at AZA Finance, Leon Issacs, Managing Director of DMA Global, and Linus Adaba, Head of Group Remittance Distribution at Ecobank lent us their thoughts and feelings on compliance and mobile money in Africa in the wake of the COVID-19 pandemic.

Muhammad M. Jagana

In larger cities and towns, there really is no issue when it comes to mobile adoption. Where we’ll face significant challenges is in the last mile of the inclusion journey; the towns or villages that are maybe 200 miles away from a major city.

How do you onboard these clients so they can use mobile money in their local shops and businesses and how will a small local shopkeeper take that payment and convert it into cash to pay their supplier? It’s one of those situations where unless everybody goes digital at the same time, there’s always going to be those at the bottom of the ladder missing out.

For these people, some of whom might not even be aware of the benefits of mobile money, it’s going to be a case of not only education but ensuring that regulators can make it easier for them. For example, in the Gambia, we have two mobile money operators and those two operators are incompatible with one another because they are direct competitors.

Rather than trying to shoehorn everyone onto the same network, we need to ensure there are regulations in place that allow for integration between different networks. It’s up to the regulators to figure out the logistics, of course, but the banks and agents need to play their part too. Something akin to the PSD2 regulations would make the most sense but realistically that’s a rather large hill to climb.

Sidharth Gautam

I completely believe that digitisation and mobile adoption is the key going forward in Africa. At the moment, cash is still king but there is a sea change on the horizon. There are hordes of challenges standing in the way of this change, of course. There are liquidity issues even on the cash pickup front, particularly in Western Africa, as well as the KYC process to sort out, user interface and customer satisfaction. It all comes into play.

There are a lot of plates that need to keep spinning, so to speak. And the regulator has to be on top of it all; the engine leading the train. It’s not an easy task to bring the offline to online puzzle together but it’s not insurmountable either.

Linus Adaba

Personally, I’ve always enjoyed working things into silos and that’s partly how I see mobile money adoption in remittance filtering through into the African market. I see one silo of mobile money that is state-led and the other that’s more private or enterprise led and we are seeing so much more innovation on the private enterprise side because of the lack of regulation.

In order for the state-led operators to catch up, they need to start investing in better compliance tools and putting good compliance managers in place. This way they can ensure people who are using mobile money are at the level of KYC that regulators expect.

When we’re talking about the last mile of the inclusion journey, as Muhammad mentioned, telecommunications companies are selling SIM cards even in the most remote villages, so the infrastructure is definitely there. The problem is that they need to subject themselves to the central bank in each country and there is a lot of technology that’s allowing nimble KYC to be done.

For remittance businesses, meanwhile, there needs to be something of a threshold. Because if it’s just remittance across borders, the full KYC protocol is simply not necessary. In this case, there could perhaps be some sort of a ‘KYC light’ solution. I also see a strong headwind in countries where you have a national ID system in place and we’re currently looking at ways to link this ID with SIM cards to help with faster and better KYC.

Oussama Kseibati

To lead on from Linus mentioning SIM cards and national ID. I think it would be hugely beneficial for the African mobile money market if there was a database such as PSD2 in Europe. With this database in place, once you’ve reached a certain compliance standard with your systems and technologies and you’re ticking the right boxes, doors can open for you automatically.

If there was a centralised database working across countries all linked to SIM cards, you’d be able to use that to do KYC. But what would need to happen first is for a standard to be implemented that will make it easier and more open for people to trade with each other. And that probably isn’t going to happen anytime soon.

For now, instant payments with instant delivery is the way forward for the region I feel. M-Pesa is a positive sign of things to come. It was a major success for Africa throughout the pandemic and the adoption of mobile wallets is continuing to rise in general. Indeed, digitally ready players have seen business growth through the roof as people are migrating towards mobile payments to remain safe from the virus. However, there has to be action in terms of regulation and regulatory frameworks.

Reaching the Great Unbanked

Everything is moving towards the digital market and many unbanked customers are using mobile platforms. That large influx and the onboarding that needs to be done is going to require a lot of compliance and a lot of work but it’s almost certainly going to result in faster, better and more affordable remittance for Africa. Given the fact that remittance rates are so high in the continent right now thanks to a heavy reliance on cash payouts and physical infrastructure, that can only be a good thing.

To read more on what our panellists had to say regarding the more specific challenges facing mobile adoption in the region, click here for our companion piece or check out the full webinar here. If you are a money service business interested in expanding into the region, meanwhile, RemitONE is an award-winning provider of MSB technology.

If you need support with all your operational needs please contact us by emailing marketing@remitone.com to see how we can support you.

Remittances: Getting digital-ready for post-pandemic recovery

The world bank has predicted that remittances are set to decline by 20% as a direct result of the pandemic, marking the sharpest decline in recent history. This is understandable on a surface level, of course, as remittance payments are most commonly sent between families and friends, and in the current climate, for migrant workers particularly, the pandemic has caused a dramatic fall in wages and employment.

However, the remittance sector is nothing if not resilient and for some, the pandemic has proven to be something of a catalyst for a sea of change that’s been simmering just under the surface for years now. Could COVID-19 be the final push the sector needs to jump off the digital cliff edge once and for all? With ‘Neobanks’ like Monzo, Starling and Revolut paving the way, the waters are not quite as untested as you might think.

Of course, our industry has various supply chain members, all of which will have a different opinion and angle on the story. As a leading technology vendor, we reached out to an aggregator (Sidharth Gautam from AZA Finance), a payment processor (David Lambert from Transact 365), an ID verification provider (Richard Spink from GBG) and a Money Transfer Operator, (Nadeem Quershi from USI Money), to ask them how they were preparing for a digital post-pandemic recovery and where they see the biggest innovations happening moving forward.

How do you see the future of the payments industry evolving?

Nadeem

The COVID crisis has had a profound impact on the escalation of digitisation in the payment industry. Our previous primary method of processing payments was rather manual, but in the wake of social distancing, we’ve been forced into ensuring our processes are more digitised. I think that’s going to have a major short and long term impact with digitisation continuing to escalate at a rapid pace.

Richard

It’s always going to be down to what the individual MTO wants to achieve when they run a compliance process. There’s a difference between just running a process and being compliant and our experience is that some businesses will want to take that seriously and others will want to just pay lip service to it. There are two reasons for that – one is that there’s a cost to being compliant and the other is that there’s a proliferation of vendors out there now. When I started in the UK 10 years ago there were perhaps 10 vendors. Now there are around 50 money transfer operators in the UK alone and hundreds globally.

How do you see the digital channel fees changing for MTOs as the channels shift from agents to a heavier reliance on digital channels?

David

The fees themselves always come down as volume goes up. When you’re talking about lower risk payment processing the margins are always going to be razor-thin. Already today I’m seeing fees online that are almost rock bottom and it’s only going to get slower. Then there’s the prospect of open banking which is going to blow everything open and remove the baseline costs even further. Ultimately it’s a competitive and a healthy environment and the fees are going to be falling but we are in this to help each other and make money. So while the fees might be coming down, we should always keep our shared end goals in mind.

Sidharth

70% of the remittance market today is cash-based but the tide is shifting and as it does the fees are going to go down. We’re already seeing it move southwards and as the 30% increases and the 70% reduces it’s going to exacerbate that reduction exponentially.

Richard

Prices will go down, of course. But they’re not going to suddenly plummet. There is a point at which we won’t go below (that rock-bottom David referred to) then there’s the cost of going digital that smaller MTOs have to consider. The price point will come down over time but then the technology you choose to invoke will change over time too.

The other thing that’s happening at the same time is that businesses are talking about digital ID. So the technologies to digitise identities is already there but the confidence to accept it probably isn’t just yet. In the next 12 months if you’re looking at how to make your process complaint online you have plenty of choices and the decision needs to be whether you’re looking for a quick fix or a process that’s scalable in the long term?

How does risk play into digitising money transfer?

Nadeem

The real question is do MTOs assume more risk online than in the traditional model? I believe that they don’t. We’re living in an age where digital risks have been largely mitigated by the complexity of new digital IDs. So I honestly don’t see it as any riskier than the traditional model of somebody visiting a brick and mortar location and presenting a physical ID. We have automated lists with regards to sanctions and screening so can build watertight systems to manage risks that are arguably just as proficient as the traditional model.

David

I partially agree with Nadeem. However, I’d argue that the moment you remove the cardholder from the equation in a physical capacity, the risk naturally increases. We can never be 100% sure on the surface if the cardholder who is making the transaction is the actual cardholder. Not if we can’t physically see them.

Where Nadeem is correct is in the responsibility of technology in ensuring those risks are reduced. If the tech is implemented correctly and the right controls are in place then there is going to be less risk. But fraudsters are very smart and they’re always getting smarter. I’ve worked in money transfer for a decade now and have seen so many different ways that fraudsters can behave – loopholes and tricks that technology can struggle to keep up with. The risks are manageable if you do it correctly but if you get it wrong then the risks can be ten times higher.

Sidharth

My response would be somewhere in between Nadeem and David’s. Our business is focused primarily on Africa and in that region, we’re seeing a lot of digital MTOs joining our platform, more and more every day. AI will definitely play a part in mitigating the risk but the risk is always going to be there. The question is how fast the technology can improve.

Richard

As soon as you’re online you’re introducing more risks, but the technology is there to mitigate the risk. As a rule of thumb, If it looks dodgy then it probably is. As long as you run a verifiable process online to mitigate those risks then it’s worth any cost. All online businesses must accept that fraud is part and parcel of the deal. As long as you accept that, go into it with your eyes open and put the right amount of resources behind it then it’s always going to be worth the risk.

Does the digital model present more opportunity for MTOs or are we operating in a saturated market?

Nadeem

The amount of MTOs that have gone digital in the last 9 months is probably more than in the last 9 years and COVID has played a major role in that. A lot of these conversions are not new entrants into the market but are existing MTOs that has been operating more traditionally and have been forced into the digital model.

David

There’s always an opportunity to be found in chaos. Throughout history, hundreds of companies have been forged in times of crisis. Disney was formed out of the 1929 depression, Microsoft came out of a major recession in the 70s and in 2008 it’s the banking crisis that kicked off Bitcoin and Fintech. The way that compliance has moved forward so fast in recent months has really spawned a rise in applications for electronic money licenses.

The implications of that are massive and have led to an environment where everybody wants to be a digital bank. It’s like when the Beatles came along and everybody wanted to be in a rock band. Now, thanks to the Monzos and Revoluts of the world, everybody wants to be involved in Fintech. This is perhaps why, now that we’re all in crisis mode, that so many MTOs are looking to upgrade their money licenses so they can perform different functions and expand into something more.

Sidharth

Asia and Africa are frontier emerging economies. Whilst the vaccine will be a reality in the western world it’s going to take a lot longer to filter into the emerging markets. Given that they are the primary markets for our industry it’s even more apparent that digital is the way to go. Because whilst the western world might be able to return to some semblance of normality sooner rather than later, the emerging markets that rely on remittance are still going to need to rely solely on digital.

Richard

In theory, as long as a financial service business has a steady platform, they can drive the business in any way they want. I think the difference is whether your focus is on driving transactions or taking the bolder step of becoming a fully regulated business. Revolut is a good example of a business that has spent all of its time and effort acquiring customers and are now embarking on the hard bit of actually becoming a proper bank.

I think that everyone would like to see an organisation do that successfully – pivot from a business that has a large number of customers into one that actually makes money from lending money. There’s an opportunity there to scale a business from an MTO into something that provides other financial services too.

Are we seeing MTOs evolve into these Neobanks or are we saying that the pie is quite big and each will have its own role within that pie?

Nadeem

We are seeing the more established MTOs move from conventional standard payments into things like e-money wallets and they are using this type of functionality as part of their wider growth plans. But generally, I think we will be seeing some form of consolidation amongst the larger MTOs. In the larger sense, the more established players have access to more resources so they will be the ones that will be moving forward.

David

Sometimes I feel like an outsider and sometimes it’s good to have that perspective where I’m not immersed deeply inside the money transfer sector. But I advise, consult and work with several different money transfer companies. One of the things that’s interesting that I see from my perspective is that everybody has their strengths and their positions within the market. If you look at companies like Small World, for example, they work with so many smaller MTOs to provide payouts and if you look at Azimo they rely on a number of different partners to help them get into certain parts of the world.

No one can do everything by themselves as one complete unit. So consolidation and licensing are interesting for me because every single MTO out there is trying to do something relatively unique. One company might be stronger in one area than another and by working together they can offer something more holistic and of greater quality overall. So I think consolidation should 100% be on the roadmap for everyone. My only fear about consolidation is that it actually shrinks the competitive element of any industry but I think that’s a little further down the line.

Sidharth

It’s already happening. Around two and a half months back WorldRemit acquired Sendwave for $500 million. This was a growth acquisition and it’s one of many floating around right now. There is also word on the grapevine that Western Union may buy Moneygram, which is one of the top three MTOs in the world.

David

Sidharth said something interesting about acquisition for growth rather than acquisition for revenue and I have seen that a lot in the payments industry. There is a huge amount of consolidation of payment service providers buying other payment service providers simply to grow because growth is so essential for a lot of MTOs, especially when we’re operating on such thin margins.

With all this technology at our disposal, why are we still having an issue with de-risking?

Richard

Since I started talking to MTOs in 2012, I’ll be honest, it’s not got any easier. The first question I ask people as a qualifying question is ‘have you got a bank account’. If they haven’t got a bank account then they’re wasting my time because I know they won’t be using our software until they get that bank account.

The big banks just won’t take the risk. It’s too much hassle and that’s a business banking problem anyway. They could easily take the risk if they choose to, it’s whether they have the resources to be able to deliver that and that’s where you’ve got the disruption coming. Can smaller banks take on that risk? Because in another sense they have less risk in it potentially going wrong.

Nadeem

De-risking has been going on for a number of years but at the end of the day, from a bank’s perspective, it comes down to purely to risk versus reward. For this reason, I don’t think you’re going to see a change in banks attitudes or habits when it comes to de-risking. David also correctly mentioned the rise of the Neobanks and some of these smaller challenger banks but they come with their own set of limitations.

What about regulators? Should the onus be on them to make sure that this continues to be a vibrant and healthy 600 billion dollar industry?

Nadeem

Regulators are there to create a framework, structure, processes and regulations. When it comes to safeguarding good practices, regulators are increasing some of these rules and regulations but can they force banks to actually support clients? I don’t think that’s their objective or their remit.

David

I don’t think it’s in the regulators best interests to push the banks, I think when a company becomes FCA regulated it has to be independent of the banks in some respect. Because, if the FCA and banks were in cahoots with each other it would be it much easier to operate but you’d also leave yourself much more open to fraud. If the two remain independent and they are independently scrutinised you have a sort of double lock system.

Sidharth

Regulators are becoming more and more progressive enablers to our industry. At least in my experience. In the UK and Europe, we have the example of open banking which is fuelling innovation and is also making the industry more compliant. All the stakeholders are becoming more and more transparent and it is helping to increase the credibility of the segments.

Africa and Asia are still very very fragmented. 54 countries with 54 different regulations. So they have a lot of catching up to do but then you can clearly see in Kenya, Uganda and Nigeria that things are moving at a very fast pace and regulators are moving likewise.

Finally, where do you think the biggest innovations will be moving forward?

David

A lot of innovation is happening right at our doorstep in the Fintech space. Payments is an ever-evolving industry. Every single day there’s a new payment method, a new way of doing things or a new market that can be exploited. Once blockchain technology has crossed over into the mainstream and people realise they can effectively move money as fast as they can send an email, that’s going to be the big breakthrough, that’s the innovation.

Nadeem

There is excitement around blockchain, digitisation of tokens and the ability to make payments instantaneously, of course. But there’s also innovation around digitised prints in terms of digital KYC and simplifying processes for consumers. I think simplification is going to be a key in terms of ensuring not only that funds are instantaneous but that the customer relationship does not simply finish at the point of collection or deposit.

Our thanks to David, Richard, Nadeem and Sidharth for their words and their time.

For more information or to speak to one of our experts please email marketing@remitone.com

R1 Webinar: The Future of Remittances

Has COVID catalysed the digital transformation of the remittance industry?

COVID-19 has fundamentally changed a lot this year. In the case of the money transfer industry, the immediate impact has not been a positive one. The World Bank has predicted that global remittances are set to decline by 20% as a direct result of the pandemic. Something needs to be done and it’s the young and nimble money transfer operators (MTOs) that are best equipped to create a new digital path in a world where physical contact is restricted.

The evidence of digital transformation

Digital transformation has been slowly changing the remittance sector for decades now and COVID has hastened that transformation. The fact is, where digital was once an option it’s now a necessity and that has completely changed the game for all banking sectors.

According to recent RemitONE transaction data trends, there has been a major acceleration of digital channel use during the pandemic. The use of physical agents, meanwhile, is down, which might seem insignificant but points to a drastic overall shift in consumer habit.

Throughout history, it’s the sectors that have been able to adapt to the times that have weathered the storms and retained their relevance. With the recession caused by COVID-19 taking a toll on the ability to send money home and remittance flows projected to decline even further by 14% in 2021, an easier, cheaper remittance solution has never been more vital.

Digital money transfer

Studies have proven that remittance not only helps to alleviate poverty in developing countries but can also lead to an increase in domestic spending. If there’s one thing we need right now it’s for people to be spending more. Digital-first MTOs are the ones ready to offer the most robust and accessible easy-to-use remittance services with fair and reliable exchange rates.

Of course, this is not a change that can happen overnight. Historically speaking, migrant communities would rely on physical money transfer services and these services have, as a result, become pillars of the community. Indeed, it’s estimated that the recipients of many international remittances are unbanked, which might go some way towards explaining why 90% of remittances currently begin and end with cash.

Does this mean it’s up to remittance operators to prove their worth and make themselves more accessible? Because digital operators that use the latest remittance software are not faster and only more affordable due to the obvious lack of overheads but have been proven to be better at evaluating customer experience and security.

Digital acceleration beyond the pandemic

It’s no exaggeration to suggest that COVID-19 changed the world overnight, but the impact on the migrant community has been under-reported. For months now, foreign travel has been almost impossible, which means migrant families have been unable to visit their families. What’s more, the pandemic has amplified the pressures migrants face in striking a balance between supporting themselves and supporting their families back home. For these families, digitally native money transfer operators will play a crucial role in redefining remittance and money transfer for a post-COVID world.

There are several benefits of digital transformation for the remittance sector for both legacy and upstart operators. Through the use of money transfer software on desktop computers and via smartphone apps, it’s never been easier and faster for customers to keep a reliable track of their remittance journey. The pandemic might have offered an opportunity for operators to use this software to foster trust and build new customer bases that keep communities connected and able to hold each other up.

This is proven by the growth of M-Pesa as the predominant payment method in Kenya. This is a digital solution that manifested because a traditional banking ecosystem was simply not accessible for a majority of Kenyans. That digital alternative quickly became the preferred option when users realised how powerful, easy, and convenient it was. Ultimately, it’s a safer, faster, and easier service that should help shoulder some of the stress that migrant families currently find themselves under.

Conclusion

Consumer preference has been shifting away from cash for years now and with many cash-based remittance solutions forced to close due to COVID-19, the future is definitely in digital. What money transfer operators and other fintech organisations need to understand is that this represents an incredible opportunity for them to prove their worth.

Borders might be closed but migrant workers still depend on remittance and if they’re going to make that switch from their old inflexible and outdated conventional means to more accessible solutions, they might need a bit of a gentle push.

To discuss your online offering with our team of experts please contact marketing@remitone.com

R1 Webinar: How money service businesses can maintain growth during a global pandemic

15:00 GMT, Wednesday 25 November 2020

Access the event today at 15:00 GMT here – https://zoom.us/j/97768332874

Join our next webinar where we will review recent challenges Money Service Businesses are facing, impacted by the global pandemic.

We will reveal how RemitONE clients have adapted to these new challenges and in doing so have maintained business growth and ensured compliance:

- Maintaining business growth – Challenging for any business impacted by the global pandemic and with the World Bank predicting global remittances will decline by 20% in 2020, it is critical that we all take action to keep money transfers flowing.

- We will share how JMMB have maintained business growth. How they have increased transaction volumes, expanded operations and scaled their business.

- Ensure compliance– Regulators have become even more stringent and we are seeing growing pressure by central banks to track inbound and outbound transactions.

- We will explain how Bank Asia delivers a robust and compliant platform. How they enforce KYC and AML procedures with ease, allowing them reduce costs and focus on other business goals.

- Licensing – A three-fold increase in new entrants to the market, judging from the number of MSB applications being submitted to regulators in different regions.

- We will reveal how Nation Transfer successfully obtained an SPI licence so they could facilitate cross border payments from the UK via digital channels.

Join our next webinar where we will discuss how we are working with clients to overcome these key challenges and take advantage of the opportunities that lie ahead!

We look forward to seeing you there.

15:00 GMT, Wednesday 25 November 2020.

Access the event today at 15:00 GMT here – https://zoom.us/j/97768332874

About RemitONE

RemitONE is a technology and business services firm that breathes innovation and excellence into the money transfer world for all types and sizes of organisations including banks, money transfer operators, micro-finance institutions, telecom firms and start-ups. Our technology allows you to manage your entire money transfer business and connect with our extensive client and partner network worldwide. Our consulting services have an impressive success rate for money service business license applications and alternative bank account solutions.

Follow us on Twitter (@RemitONE) and LinkedIn (RemitONE) for the latest industry updates.