New White-Label Online Platform: Redesigned to Scale Customer Loyalty and Growth

Add powerful money transfer capabilities to your website — without the complexity.

Our new Online Remittance Manager (ORM) is a fully white-label web application that lets your customers send money securely and easily — all under your brand, without leaving your site.

Built on a foundation of powerful features, now enhanced with a seamless new design.

Your brand will sit proudly on a modern, intuitive platform that makes sending money simple — helping you build loyalty and drive growth.

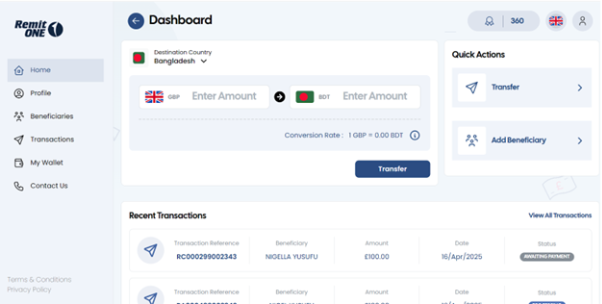

Instant, Simple Money Transfers

From the moment customers log in, they see what matters most: Send Money.

Quick Actions let them add beneficiaries without hunting through menus.

Recent transactions are easy to review at a glance.

Navigation is streamlined on the left-hand side for effortless access.

How much time could your customers save with this design?

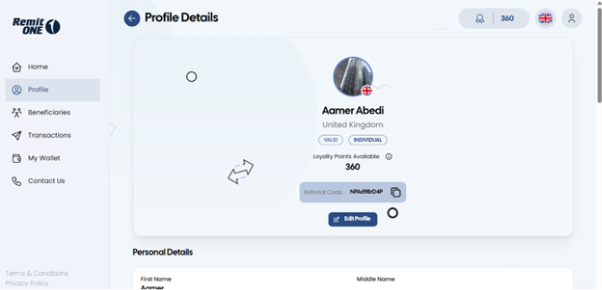

Enhanced Customer Profiles for Better Insights

The Profile section now gives a richer overview of each customer—helping you serve them better. Instantly see key details like available discount codes, submitted ID proofs, and whether they’ve completed their KYC checks—all in one place.

What would better visibility mean for your client relationships?

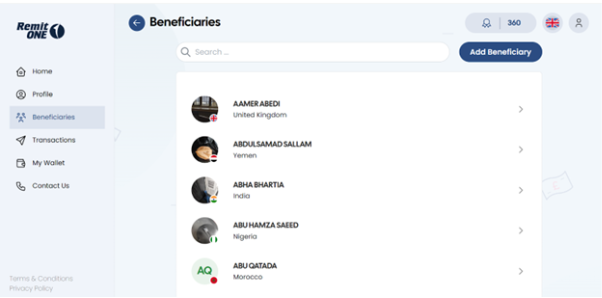

Quick Access to Saved Beneficiaries

The Beneficiaries section lists all saved contacts alphabetically, so customers can quickly find who they’re looking for. With the built-in search, there’s no need to scroll endlessly—just type, find, and send in seconds.

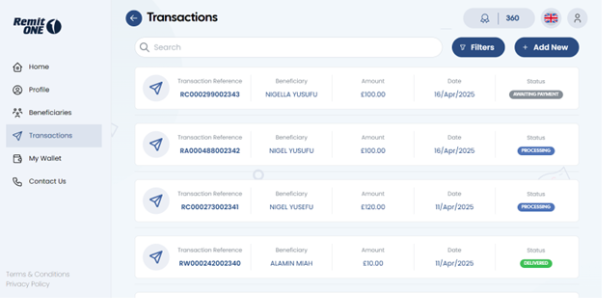

Detailed Transaction History with Smart Filters

Customers see every transfer in a clean timeline. Clicking on any transaction reveals a full breakdown—including fees, status, and more.

Smart filters make finding specific transactions easy: By date, type, or status.

And with the “Add New” button, they can jump straight into sending money again, with no backtracking needed.

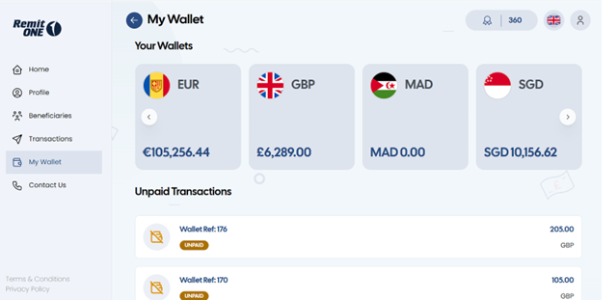

Multi-Currency Wallets Made Easy

The My Wallet section displays all the wallets your customer holds across different regions, along with the balance in each one. The left and right toggle arrows offer a smooth way to scroll through the full list—making it easy to manage multiple wallets without overwhelming the screen. It’s a user-friendly experience that keeps everything organised and accessible.

Below, customers can also view a history of unpaid transactions, so nothing slips through.

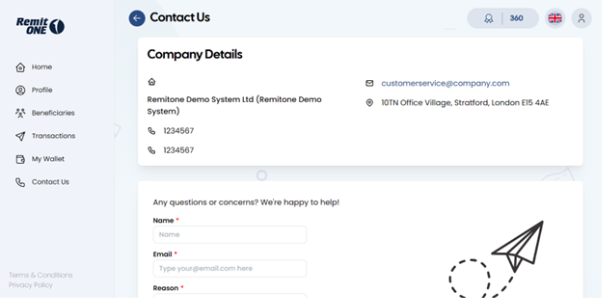

Easy Customer Support Access

Finally, we’ve reached the Contact Us page—an essential space where customers can reach out whenever they need support. It’s not just a lifeline for them, but also a valuable channel for you to stay informed about any issues and respond quickly.

At the top, customers will find your company’s contact details, with an enquiry form below as a convenient alternative for getting in touch.

Ready to impress your customers with a smarter, sleeker platform?

Our redesigned Online Platform and Mobile App aren’tjust better looking — they’re built to help you:

- Deliver a world-class experience

- Scale faster

- Work smarter

Book a demo today to explore the platform firsthand, get expert answers to your questions, and discover how to turn clicks into conversions — and customers into loyal fans.

How to Build a Leaner, Smarter Money Service Business in 2025

In an era of rapid regulatory change, rising customer expectations, and digital disruption, how can money service businesses (MSBs)—companies that facilitate the transfer, exchange, or payment of money—not only survive but thrive?

In our recent webinar, we gathered our top experts and unpacked the most pressing challenges facing MSBs today and shared proven strategies to help you scale, streamline compliance, and embrace innovation.

Here are the top takeaways:

1. Scale Smarter with our All-in-one Hub

A major pain point for MSBs is integrating with multiple systems and partners from send and payout providers to value-add services like ID verification platforms, open banking tools, and payment gateways.

RemitONE Hub™ solves this by offering two flexible options: connect via a single API or use our ready-made interface. Either way, you gain instant access to a global network of payment companies with the likes of Visa, Mastercard, Orange, MoneyGram, and many more.

With access to over 2.5 billion bank accounts and 3 billion wallets, the RemitONE Hub™ gives you the tools to scale without stress. You stay in control of your payouts, partner terms, and operations—all from one place.

We’ll help match you with the right partners based on your target corridors and budget to help meet your goals. What normally takes years, we help you achieve it in a few months.

2. Shortcut to Launch into New Corridors

Expanding to new corridors can feel like a maze of licences, banks, and paperwork. But it doesn’t have to be that way.

With our Remittance-as-a-Service (RaaS), you can plug into our network of licensed partners across the UK, EU—and soon, the US and Canada. That means you can go live faster, spend less upfront, and stay fully compliant—without going it alone

3. Stay Compliant with Compliance Manager™ (COM)

Compliance and fraud prevention remain top priorities for MSBs. Our Compliance Manager™ (COM) automates 80% of those repetitive manual checks, runs real-time KYC/AML screening across 350+ global sanctions lists, and helps you monitor risk scores, transaction patterns, and suspicious activity.

And it’s not just for MSBs. For central banks and regulators, COM offers live visibility into incoming and outgoing remittance flows—making it easier to track volumes accurately and close those reporting gaps.

In short? You stay compliant, catch fraud early, and get to focus on growing your business.

4. Reduce Costs and Settlement Delays with Open Banking

We know how frustrating slow settlements and high fees can be—especially when you’re trying to keep things efficient. That’s why we support open banking. You can tap into direct bank-to-bank payments, which means faster processing times, fewer card-related fees, and reduced friction that often comes with traditional payment methods. We’ve already rolled this out across the UK and Europe through our partners, and it’s making a real difference.

Even in countries without open banking, we provide alternative integrations with local processors.

5. Offer Multifunctional Wallets for the Future of Finance

Let’s be honest—digital wallets aren’t optional anymore. They’re a core part of how people move money today, and we’re making sure our clients are ready for that shift.

We support everything from peer-to-peer transfers, bill payments, airtime top-ups, prepaid cards, and wallet-to-wallet transactions. Whether your customers are paying for groceries, sending money to family, or topping up Netflix—we’ve got it covered.

We’ve also made sure our wallets connect to telcos, banks, and blockchain partners all with compliance built in from the get-go.

It’s all part of how we’re helping MSBs stay relevant, inclusive, and ready for whatever comes next.

6. Leverage a Flexible Platform Built for Growth

One recurring theme throughout the webinar: flexibility is key. Whether you’re a startup finding your footing, a licensed MTO looking to scale, a send or payout partner, a central bank, or a sub-account issuer like an e-money institution, your needs will keep evolving. That’s why we’ve built our platform to move with you. Our white-label solution adapts to your regulatory landscape, your operations, and your goals—without locking you into one way of working.

Because here’s the thing: if your platform isn’t flexible, you can’t adapt. And if you can’t adapt, you’ll get stuck—while your competitors sprint ahead.

Worse still, you’ll waste valuable time patching together workarounds instead of moving forward. We’ve seen it too many times, which is why we’ve made it our mission to keep things open, partner-friendly, and ready for what’s next.

Real growth happens when your platform moves with you—not against you.

Ready to Future-Proof Your Business?

The remittance and payments landscape is shifting fast, and the businesses that thrive are the ones that stay agile, compliant, and connected.

At RemitONE, we’re not just building software. We’re helping MSBs grow smarter, launch faster, and operate with confidence, no matter where you’re headed next.

If any of these challenges sound familiar, or if you’re curious about what’s possible with the right tech and support behind you, we’d love to talk.

Book a free consultation call with our expert consultant or drop us an email for any questions at: sales@remitone.com

Trump’s Threats to Cross-Border Payments: What It Means for Your Business

It’s been a short while since Trump stormed back into office, and he’s already shaken things up with his hard-hitting policies—and, as always, he’s not one to shy away from bold and upfront decisions. But with every action comes a ripple effect, and in the world of cross-border payments, those ripples are turning into shockwaves. From proposed remittance taxes to intensified compliance risks, Trump’s latest moves are shaking up how money flows in and out of America.

So, what does this mean for businesses, migrants, and economies relying on these payments? Let’s find out.

- Will Deportations of Migrants Impact Remittances? Here’s What the Data Says

Mexicans, a huge diaspora, and one of the major remittances senders in the US, but we may see stricter immigration policies putting this financial lifeline at risk. The “Remain in Mexico” program has already led to nearly 11,000 migrants being sent back, potentially reducing the number of workers in the U.S. and, with them, the flow of cross-border payments. Since Trump’s arrival, 23,000 arrests have been made and 18,000 deportations, whilst it has risen significantly compared to the Biden administration it still remains lower than the peak levels seen during the early crackdown of Trump’s first term.

So, what does this tell us? When Trump first took office, deportations surged as part of his hardline immigration stance. But over time, the wave slowed down. Now, despite his promise to deport 11 million people, the sheer complexity of the process appears to make that goal unlikely. In fact, this could even open a window for some undocumented migrants to secure legal status. But let’s say, hypothetically, mass deportations would happen—would remittances take a massive hit? Not necessarily. Many undocumented migrants are low-value remitters, meaning their contributions wouldn’t cause a drastic drop. What would shake remittance flows, though, is something much bigger: a tax on remittances.

- Will a Remittance Tax on US-Latin America Transfers Disrupt the Market?

The proposed 10% remittance tax from the US to Latin American regions is an effort to minimise illegal immigration but can cause a significant dent on transactions, impacting money transfer operators, banks, and other players in the payments ecosystem by reducing revenue and lowering demand in certain corridors.

For countries like Mexico, El Salvador, and Haiti—where remittances inject nearly $150 billion annually, this could be a devastating blow. Families who depend on these funds risk losing critical income, putting entire economies under strain.

If implemented, Money Service Businesses (MSBs) may have no choice but to raise fees, potentially driving customers toward alternative solutions like digital wallets and crypto. Interestingly, Trump seems to support crypto, so could this be the turning point that finally makes it more secure and mainstream?

- Trump and Stablecoins: A Game-Changer for Cross-Border Payments?

There’s hope on the horizon—Trump’s pro-stablecoin stance could be the catalyst to reshape cross-border payments. While Trump has halted any action to progress America’s CBDC, he’s taken more steps to advance the crypto movement. In a tweet, he unveiled the U.S. Crypto Strategic Reserve, which will include XRP, SOL, and ADA, with Bitcoin (BTC), Ethereum (ETH), and other key cryptocurrencies that will be added to “the heart of the Reserve.” Since the announcement, the value of the first three coins surged by 62%, while BTC and ETH have climbed up by 10%. This momentum is pushing forward Trump’s goal of making the U.S. the “crypto capital of the world.”

Two posts by Donald Trump on Sunday, March 3, 2025, on his Truth Social account.

So, what does this mean for remittances? Stablecoins offer faster, cheaper, and more accessibility, eliminating high fees and long processing times, making this a more attractive alternative to existing transfer methods to senders.

Of course, regulation follows. Trump’s administration has called for a federal regulatory framework for digital assets to bring clarity. If well executed, this could boost financial inclusion and drive crypto adoption, but if it becomes too strict, it can do the opposite, where it stifles innovation and progression.

- Crypto in Crisis: What’s shaking the market?

The cryptocurrency market took a plunge over the weekend, and while crypto is no stranger to volatility, this time the drop wasn’t just about digital assets—it was about politics, economics, and the shifting global financial landscape.

A major trigger was the Trump administration’s new tariff hikes on imports from Mexico and Canada, which sent investors retreating from risky assets like Bitcoin, creating a domino effect across the sector. Then there was the regulatory uncertainty. The U.S. government’s new restrictions on crypto exchanges and stablecoins fuelled distrust, prompting even more selloffs. On top of that, fresh inflation data and Trump’s aggressive trade policies led to a reassessment of potential Federal Reserve interest rate cuts, putting even more pressure on risky assets like crypto.

Ironically, part of the turmoil can be traced back to Trump’s own cryptocurrency summit on March 7. The announcement of a strategic bitcoin reserve—a government-controlled stash of digital assets initially caused Bitcoin’s price to drop by 6%. While the move signalled greater government involvement in crypto, it left many investors questioning what that would actually mean in practice. The market’s uncertainty around this policy likely contributed to the larger crash that followed.

- Stricter Compliance: A Roadblock for Remittances?

The designation of cartels as terrorist organisations, combined with tighter immigration policies, is set to intensify compliance pressures on MSBs. They must now exercise even greater due diligence to avoid any unintended links to sanctioned groups.

For migrants, this means longer wait times, extra fees, and fewer options to send money home. If traditional corridors start shutting down, people will have no choice but to look elsewhere, whether that’s the age-old hawala system or the rising use of crypto and stablecoins, a shift that could play right into Trump’s pro-digital currency agenda.

Whereas for giants like Western Union and MoneyGram, who move billions to Latin America, the stakes are high. Stricter AML (Anti-Money Laundering) and KYC (Know Your Customer) regulations will be unavoidable, but for some financial institutions, the risk might be too much. We’ve seen this play out before where banks pulled out of Somalia’s remittance corridors when terrorist groups gained traction, leaving thousands stranded without access to funds. Could Latin America perhaps face the same fate?

Keeping up with ever-changing regulations is more than just a headache—it’s a matter of survival. A single compliance slip-up can trigger heavy fines or, worse, force a business to shut its doors entirely. Yet, many companies still juggle multiple software tools, manually stitching together fragmented systems to stay compliant.

This approach isn’t just inefficient; it’s risky. When regulations shift overnight, you need a solution that evolves with them. That’s why we built an all-in-one platform with compliance at its core. Unlike other providers, we continuously adapt to market trends and regulatory changes, ensuring you aren’t left scrambling when new rules emerge.

Take our Liveness feature for example. With biometric-powered selfie checks, remitters can instantly confirm their identity—cutting fraud risks while keeping regulators satisfied. Plus, through our platform, regulators and central banks can track all inbound and outbound transactions, ensuring total transparency.

It’s this kind of innovation that makes compliance less of a burden and more of a competitive advantage.

So if you want to streamline your operations and power your growth, book a free demo with us and let’s discover how.

RemitONE Webinar: Future-Proof Your Money Service Business

Future-Proof Your Money Service Business: Tech-Driven Solutions to Cut Costs, Boost Transactions, and Drive Growth, Tuesday 8th April at 15:00 GMT.

In today’s challenging remittance landscape, rising operational costs and declining transaction volumes are putting pressure on Money Service Businesses like never before. Staying ahead requires smart, technology-driven strategies—and this webinar will show you how.

Join us as we uncover practical solutions that will empower your business to reduce costs, increase transaction volumes, and maintain a competitive edge:

- Connect and Scale Effortlessly: Leverage RemitONE’s connections to integrate seamlessly with your supply chain members and partners.

- Expand Into New Markets: Access new corridors from the UK and Europe with plug-and-play solutions like Remittances as a Service (RaaS), without the need for a license or bank account.

- Boost Security and Speed: Harness the power of open banking for faster, cheaper and more secure transactions.

- Enhance Compliance and Risk Management: Adopt liveness checks to streamline compliance, mitigate fraud risks, and ensure regulatory adherence.

- Future-Proof Your Business: Explore blockchain, stablecoins and other digital innovations designed to increase efficiency.

Don’t miss this opportunity to gain practical insights that can help your Money Service Business. Spaces are limited, so register today to avoid disappointment. Register here – https://events.teams.microsoft.com/event/93c0ed25-77aa-4b24-a749-ab16b888b23b@36d5614f-f651-4945-9632-7053acdae73a

Unlock Faster, More Secure Payments with RemitONE’s Open Banking Solution

We’re excited to introduce the latest enhancement to our RemitONE Money Transfer Platform: the RemitONE Open Banking Solution. Competitively priced and designed to offer businesses a faster, more secure, and seamless payment experience, this powerful new feature ensures maximum value for our clients through advanced open banking capabilities.

Open banking is revolutionising the financial industry by allowing businesses to connect directly with their customers’ bank accounts to initiate payments. By bypassing intermediaries such as card networks, open banking delivers numerous benefits:

Key Benefits of the RemitONE Open Banking Solution:

- Faster Transactions: Payments are processed almost instantly, providing businesses with quicker access to funds and improving cash flow.

- Enhanced Security: Secure, direct payments minimise the risk of fraud and chargebacks, giving both businesses and customers peace of mind.

- Cost Efficiency: Open banking eliminates many fees associated with traditional card payments, making it a cost-effective option for businesses of all sizes.

- Streamlined Customer Experience: Customers can authorise payments through their mobile banking apps, ensuring a smooth and frictionless checkout process.

Our RemitONE Open Banking Solution, powered by RemitONE’s award-winning technology, seamlessly integrates into the RemitONE Money Transfer Platform. This plug-and-play solution allows clients to quickly enable open banking without the need for complex technical integrations.

This enhancement underscores RemitONE’s commitment to staying at the forefront of payment innovation, equipping our clients to thrive in a rapidly evolving digital economy.

Get Started Today

Take advantage of this feature to unlock the full potential of open banking for your business. Book an exploratory call today using the link below to learn how you can implement this solution and deliver a superior payment experience to your customers!

How Banks Can Reclaim Their Role in Cross-Border Payments with RemitONE

Banks, once the cornerstone of international payments, are finding themselves sidelined. Senders and receivers have now joined forces, pushing banks out of the equation.

But all is not lost. By embracing cutting-edge tools and software, banks can avoid being bypassed by larger MTOs and telcos. By connecting via a simple API to the RemitONE Hub™, they gain access to a multitude of MTOs, banks, and telcos worldwide, enabling them to send or receive various payment types, including cash, bank account, airtime, utility bills, and mobile wallet payments.

The Challenge: Banks on the Sidelines

The traditional banking model for international money transfers is facing significant disruption. People now have access to digital services that make transfers quick and easy with just a tap on their phone. Fintechs and money transfer operators (MTOs) help senders move money faster and cheaper, while aggregators and telecoms ensure it reaches even the most remote places.

Which leaves the lingering question: Where does that leave banks? How can they stay relevant in this shifting landscape?

The Solution: The RemitONE Hub™

RemitONE offers a powerful solution by acting as a bridge between banks and the wider fintech ecosystem.

The RemitONE Hub™ is a secure, flexible platform to manage and process money transfer transactions. Powered by modern technology, it offers real-time transaction monitoring, tracking, detailed reporting, and customisable features, all offered within a white-labeled solution.

What makes the RemitONE Hub™ stand out?

- Relevance: connects all key entities in the supply chain—MTOs, banks, and telecoms—ensuring that every participant benefits from the ecosystem.

- Flexibility: seamlessly integrates with existing systems, allowing banks to plug in with minimal disruption. Alternatively, it can replace outdated money transfer platforms, and infrastructure, offering unmatched adaptability.

- R1 EcoSystem™: gain access to the expansive RemitONE network to open doors into untapped corridors and unlock fresh revenue streams. Take a look at a quick snapshot below:

Here’s how RemitONE Hub™ reconnects banks to the global money transfer network:

1. Connecting Sending Partners

Sending Partners: The entity responsible for originating the fund transfer, whether through a digital platform or traditional method.

On the sending side, the RemitONE platform integrates with:

- Fintechs

- MTOs

- Aggregators

2. Empowering Receiving Partners

Receiving Partners: The entity that receives the funds on behalf of individuals or businesses, whether through a digital platform or traditional method.

On the receiving side, RemitONE connects banks to:

- Fintech

- MTOs

- Aggregators

- Telecom Operators

This interconnected framework ensures that banks remain an integral part of the financial journey, from sender to receiver.

With RemitONE’s all-in-one system, the complexity of managing multiple platforms is eliminated, saving your team valuable time and reducing the risk of human error. With fewer systems to manage, your processes become more efficient, allowing your bank to operate smoothly, stay ahead of competition, and remain fully compliant—staying firmly in the good books of regulators.

Conclusion: The Future of Banking in Cross-Border Payments

The financial world is moving forward, and so must banks. By embracing platforms like RemitONE, banks can transform potential challenges into opportunities, becoming central players in the global money transfer network once again.

We’ve already empowered leading banks like Stanbic Bank, Banco do Brasil, Attijariwafa, and UBA—and you can be next.

The RemitONE Hub™ is not just a solution; it’s a lifeline for banks striving to stay ahead in a rapidly digitising world. With its ability to connect banks to the innovators driving the money transfer revolution, RemitONE ensures that no one gets left behind.

Book a FREE consultation with our expert consultants, and let’s get your bank back in the cross-border payments game.

We’re Attending CrossTech World 2024 | 19-21 November 2024

We’re excited to announce that the RemitONE team will be heading to Miami, USA, for the upcoming CrossTech World 2024 event. This is an incredible opportunity for us to connect with potential partners and reconnect with our valued clients who have supported and grown with us along the way.

If you’re attending CrossTech, we’d love to meet up and explore how RemitONE’s cutting-edge software and tools could elevate your business. Whether you’re interested in expanding into new markets through our extensive network of banks, telecoms, and money transfer operators, or keen on participating in our upcoming events—such as those focused on emerging opportunities in Saudi Arabia. Let’s make the most of this event together.

To schedule a meeting with the RemitONE team in advance, simply reach out to us at sales@remitone.com.

We’re looking forward to connecting with industry peers and exploring new avenues for meaningful collaboration.

Innovation in Payments and Remittances (IPR) Global 2024 Award Winners!

Earlier in the month, we gathered the top global companies in the Remittance and Payments space in our annual IPR Global 2024 event. On day two, we hosted our award ceremony to honour the game-changers and trailblazers who are pushing the industry forward in exciting new ways.

The RemitONE team is excited to unveil the winners who took home the trophy, along with the honourable mentions — those who came close and deserve recognition for their impressive efforts:

Company of the Year 2024

Winner: Flutterwave

Honourable mention: Jamuna Bank PLC. Bangladesh

Social Impact Award 2024

Winner: Ding

Honourable mention: United Bank Limited

Exceptional Customer Experience Award 2024

Winner: Cauridor

Honourable mention: Neo Money Transfer

Start-up of the Year Award 2024

Winner: Sikoia

Honourable mention: WeWire

Innovation Award 2024

Winner: Uniteller Financial Services

Honourable mention: Tiketi Rafiki

All entries were thoroughly evaluated by our esteemed judges comprised of global senior experts in the payments and remittance industry:

- Leon Isaacs, CEO & Founder, DMA Global

- Kathryn Tomasofsky, Executive Director, MSBA

- Osama Al Rahma, Advisor, Board of Foreign Exchange & Remittance Group (FERG)

- Veronica Studsgaard, Founder & Chairman, IAMTN

After the initial assessment, the award finalists were unveiled in August 2024. This was followed by the second stage, during which the judging panel reviewed all the finalist entries and selected the winners in each category through an anonymous scoring method.

From left to right pictured: (Top left) Alpha Diallo, Marta Pillon and Rob Ayers, (Top middle) Lindsay Lehr, Bob Dowd and Olivia Biviano, (Top right) Alberta Guerra and Lindsay Lehr, (Bottom left) Leon Isaacs, Sid Gautam, Shikesha Panton, Noel Ozoemena and Sadat Choudhury, (Bottom right) Bob Dowd, Olivia Biviano, Alpha Diallo, Marta Pillon, Albert Guerra, Noel Ozoemena and Shikesha Panton.

About Innovation in Payments and Remittances (IPR)

In 2018, RemitONE launched Innovation in Payments and Remittances (IPR) to bring together various industry supply chain members to drive positive change. Through events and research reports, IPR unites senior business leaders dedicated to enhancing the industry, enabling them to think big, share best practices, engage, learn, discover, create opportunities and shape change. With the power of collective insight, we can push innovation and industry growth boundaries and benefit from better outcomes.

The IPR events are organised throughout the year to help industry stakeholders, visionaries and business leaders make informed decisions that ultimately benefit the consumers.

About RemitONE

RemitONE is the leading provider of end-to-end money transfer solutions for banks, money transfer operators (MTOs) and fintech start-ups worldwide. Our award-winning money transfer, compliance software products and consulting services – including MSB licensing, bank account provisioning and connections to our clients and partners – are tailored for the global money transfer market.

Organisations of all sizes use our platforms to run their remittance operations with ease and efficiency by reaching out to their customers via multiple channels, including agent, online and mobile.

For more information, or to access all the photos from the IPR Awards ceremony, please contact marketing@remitone.com

Innovation in Payments and Remittances (IPR) Global 2024 Awards | Finalists Announced!

We are thrilled to announce our finalists for this year’s IPR Awards. The IPR Awards is a prestigious event celebrating the exceptional achievements of the money transfer and payments community’s best and brightest.

This year, we introduced five unique award categories including:

- Innovation Award

- Exceptional Customer Experience Award

- Company of the Year

- Social Impact Award

- Start-Up of the Year

IPR Award Ceremony

Get ready for an unforgettable evening at the IPR Global 2024 Awards Ceremony in London on Tuesday, 17th September! Join us as we celebrate excellence in our industry with the much-anticipated announcement of our prestigious award winners.

Enjoy a vibrant standing reception with delightful drinks, delectable canapés, and the chance to connect with top professionals in the field. This is your moment to connect with industry leaders and be part of a night that promises excitement, recognition, and inspiration.

Don’t miss out on this special opportunity—secure your ticket before they’re gone: https://global2024.ipr-events.com/register

Congratulations to all the shortlisted companies

Innovation Award

- Tiketi Rafiki

- UniTeller Financial Services

- LASCO Financial Services Limited

- Neo Money Transfer

- eSIM Go

- Jaudi (Transfapay)

Exceptional Customer Experience Award

- Relianz Forex Limited

- Ebixcash World Money Limited

- Cauridor

- Neo Money Transfer

Company of the Year

- SUNRATE

- JAMUNA BANK PLC, Bangladesh

- Flutterwave

- Remit Choice

Social Impact Award

- Xpress Payment Solutions Limited

- SIAO Partners

- Ding

- SolutionsAe, Inc

- United Bank Limited

Start-Up of the Year

- WeWire

- Sikoia

Congratulations once again to all the finalists! We look forward to seeing you at the IPR event, where we’ll be announcing the winners.

If you haven’t already, register here to secure your spot: https://global2024.ipr-events.com/register

Flutterwave: Simplifying Cross-Border Settlement for Multinationals in Africa

This article is brought to you in partnership with Flutterwave, written by Sid Gautam, SVP–Enterprise at Flutterwave.

Having trouble transferring money for your business from Africa across borders? You’re not alone. International business transactions can seem like an overwhelming task due to the hidden fees and complications that are frequently involved with cross-border settlements. No more worries, Flutterwave provides an easy and cost-effective answer to your international settlement needs.

Recently named Fast Company’s Most Innovative Company in Europe, Middle East, and Africa, Flutterwave stands out as Africa’s leading payments technology company, providing an efficient and transparent cross-border payment solution. The company has established a solid reputation with over 630 million transactions worth more than $31 billion in total payment volume, and 20 million+ API calls per day.

Seamless Onboarding Processes

On the eight-year journey of simplifying payments for multinationals in Africa and beyond, Flutterwave has learned and we have adapted our onboarding processes to be straightforward with 24/7 support always available throughout the process. Our Know Your Business (KYB) process is enhanced to get you set up quickly and efficiently. This follows with other important mechanisms needed to ensure your operations are live and running in no time within stipulated regulatory requirements.

Extensive Reach and Settlement Expertise

Leveraging an extensive payment infrastructure network spanning over 30 African countries with a presence in the UK, US, and EU, Flutterwave is the cross-border payment partner of choice in Africa. Our settlement solution facilitates seamless payment operations for multinationals across Africa and African businesses growing globally.

Currently, we serve merchants across several industries: payments, hospitality, ride-hailing, aviation, gaming, logistics, and digital infrastructure to mention a few. With support for multiple currencies as well as local and international payment methods such as mobile money, bank transfers, cards, and Google Pay, your larger enterprise will be in the capable hands of our cross-border payment solutions facilitating fast, transparent, and cost-effective payment solutions.

Regulatory Compliance and Maximum Security

At Flutterwave, operation excellence and minimizing counterparty risk are our top priorities. Strict adherence to regulatory compliance through owned licenses and a network of partners across several countries within and outside Africa means cross-border transactions are settled within relevant payment policies and regulations. To ensure maximum security for merchants’ data and funds, we have risk and compliance systems and teams across several countries carrying out extensive compliance checks to mitigate anti-money laundering (AML) and combating the financing of terrorism (CFT) risks.

We also invest heavily in payment infrastructure security such as maintaining the highest PCI-DSS & ISO 27001 certifications, in line with global best practices. This ensures that whether managing B2B first-party treasury flows or third-party supplier payouts, Flutterwave’s cross-border payments adapt to specific business needs legally and securely.

In Conclusion: with Flutterwave, enterprises can streamline their cross-border settlements, ensuring speed, transparency, and cost-effectiveness. Join global merchants such as Uber, Worldpay, Piggyvest, Bamboo, Air Peace, Microsoft, and Flywire running their cross-border settlement efficiently and securely from Africa to the world and vice versa. Let’s talk!